Increasing local government debt in China has triggered concerns over the sustainability of local public finances. The link between local governments and shadow banking has led to widely varying market estimates of local government debts, ranging from 10 to 50 trillion renminbi. Growing investor concern has convinced the central government to conduct a thorough investigation of local government debts. China’s National Audit Office (NAO) announced on July 28 that it will conduct an audit of government debts at all five levels of the government – central, provincial, city, town, village – in order to estimate their size and the potential financial risks. The primary focus of this audit is debt related to infrastructure including railways and subways, local government financing platforms (LGFPs) and projects backed by the land transfer revenues. All transactions and related ledgers are expected to be audited individually, and the audit report is expected to be sent to the State Council before the middle of October.

How serious is the local government debt issue?

The most recent official estimate of the local government debts outstanding was 10.7 trillion renminbi in 2010 based on a report released by NAO in March 2011. The estimate should be the lower bound of the coming estimate, as local government debts have surged significantly, along with shadow banking, for the past two years. Moreover, the coverage in the new estimate is more complete, including debts at the village level. Bank loans to LGFPs hit 9.59 trillion renminbi in Q1 2013, 30 percent up from that in Q4 2009, according to statistics from China Banking Regulatory Commission. NAO conducted another auditing program on 36 provincial capital cities earlier this year and reported their debts totaled to 3.85 trillion renminbi and 9 cities’ debt-to-GDP ratio exceeded 100 percent by 2012. Names of those 9 cities were not disclosed, but the market has narrowed down the list to 10 cities including Nanjing, Chengdu, Guangzhou, Hefei, Kunming, Changsha, Wuhan, Harbin, Xian and Lanzhou.

Based on our grassroots survey recently, we found the debt-to-GDP ratio of the cities with sound financial positions ranged from 20 to 40 percent, while the ratio was up to 80 to 120 percent in cities with serious problems. As a whole, our best guess on the outstanding of overall local government debts is 40 to 60 percent of GDP, in other words, about 20 to 30 trillion renminbi. Some LGFPs including Shanghai, Yunnan and Shanxi have encountered difficulties repaying principle and have requested to extend loan maturities. Besides the size of the debt, the mismatched structure of the local fiscal position is another concern. Based on the NAO report in 2011, by the end of 2010, 53 percent of local government debts had 3-year maturity, while 60 percent of investments on infrastructure projects had 10-year maturity. The most pressing concern now is not insolvency but liquidity.

China's local government debts remain, in our view, are manageable zone despite their large size and mismatched structure. Unlike those in the US, Chinese government owns a large amount of assets including infrastructures, buildings, natural resources, and enterprises such as SOEs and collective firms. According to the estimate at the national balance sheet published by Chinese Academy of Social Sciences (CASS) in 2012, at the end of 2010 the Chinese government’s operating assets totaled to 21.5 trillion renminbi, 47.4 percent of which belonged to the local governments. The government’s non-operating assets amounted to 7.8 trillion renminbi, and natural resources totaled 44.3 trillion renminbi. Furthermore, China’s government tax revenues have grown steadily thanks to rapid economic growth, which doubled in the past five years and reaching 10.1 trillion renminbi in 2012. This means that there is the possibility of “growing out of the debt.”

Overall, the local government debt issue is serious but remains manageable. However, immediate actions are needed to control the situation before any potential defaults.

Measures to resolve the local government debt issue

Deleveraging is the priority in solving the local government debts. It is critical to set up a deficit and debt cap for China governments to establish a sound fiscal position. The Stability and Growth Pact in Euro zone requires all members to have deficit below 3 percent of GDP and public debt below 60 percent of GDP (Maastricht criteria). It could be a good reference for China to apply 60 percent of GDP as the safe line for the central government. And the cap of debt for the local governments should be lower considering their limited access to resources, thus a range of 40 to 60 percent is likely to be an appropriate. Besides the debt cap, an explicit timetable to achieve the target is equally important in order to give the local governments a real push to deleverage within the time framework.

Once the debt cap is established, some measures including selling government assets, securitizing debts, wiping off by the central government should be taken immediately in order to quickly lower the leverage rates below or close to the target rates. Other measures including issuing local government bonds, levying property taxes and rebalancing expenditures will be long-term solutions for a healthy and sustainable local fiscal position.

Short-Term Measures to Deleverage

Sell part of local government assets

Selling off of assets is a fastest way to deleverage in the public sector, which is particularly necessary for those with debts seriously above the cap. It could work well for the cities with good economic foundation and high quality assets, mainly located in the Yangzi river delta and Pearl River Delta. For example, the government of Nanjing, a highly indebted capital city of Jiangsu Province, likely had debt over its 720 billion renminbi GDP by 2012 and owns 331 billion renminbi in assets according to the statistics of the Nanjing State-owned Assets Investment Management Holdings Group. Partly privatizing these government assets, especially under performing operating assets, could help deleverage as well as improve management efficiency.

Restructure existing debts via the big four asset management companies

Restructuring existing debts is another solution. In 1999, China restructured 1.4 trillion renminbi nonperforming loans of the four major state owned banks via four asset management companies (AMCs) including Huarong, Cinda, Orient and Great Wall. The initial missions of the four AMC is now completed and restructuring local government debts could bring them a new line of business. Transferring nonperforming loans to the AMCs at a discounted price and negotiating an extension of loan maturity are potential solutions (80 percent of government debts are bank loans). It might increase moral hazard to some extent, but it is a reasonable one-time choice to quickly improve the overall fiscal position of the local governments.

Direct support by the central government

It is possible for the central government to help some local governments pay part of their debts, especially for those located in the middle or western regions. It was not uncommon before 2003, when local governments in those regions faced financial difficulties and had no land sales proceeds available. For example, the central government financed the local governments with proceeds from treasuries issuance with a total of 40 billion, 25 billion and 25 billion renminbi in 2001, 2002 and 2003 respectively.

Long-Term Measures to Improve Local Fiscal Positions

Allow the local governments to issue bonds

The local governments are not allowed to issue bonds directly in China. What they can do after 2009 is to submit applications to the central government, and the central government will issue bonds on behalf of them if approved. In this case, the annual quota is restricted, the procedure is long and maturity options are limited. For example, the annual quota for the year of 2011 and 2012 were 200 billion and 250 billion renminbi respectively, while expenditure of local governments totaled to 5.25 trillion and 6.16 trillion renminbi respectively. The maturity options are limited to only two choices – 3-year and 5-year bonds. A pilot program of 7-year maturity was launched in 2011 for Shanghai, Zhejiang, Guangdong and Shenzhen followed by Jiangsu and Shandong in 2013. The relatively short maturity makes it hard for the local governments to fund long-term infrastructure projects such as roads, bridges and subways. As a result, a large proportion of local government bonds issued in 2012 were used to repay 3-year bonds issued in 2009. For example, only 1.5 out of the 7 billion renminbi in local government bonds issued by Gansu province in 2012 were for new investments.

Given the restrictions of bonds issuance, LGFPs issued a high quantity of city investment bonds in the interbank market for the past three years to finance infrastructure projects. Especially in 2012, the city investment bonds issued were 636.8 billion renminbi, increasing the outstanding amount to 1.4 trillion. This was about 2.5 times higher than 2010, according to the data released by China Central Depository & Clearing Company. The lack of transparency over the ultimate borrowers of these city investment bonds has intensified market concerns of potential defaults amid a weak economy.

Overall, allowing the local governments to issue bonds directly could clearly identify the ultimate borrowers and make the government budget more transparent. The local governments should be incentivized to take responsibility for the bonds issued.

Levy property tax

Property tax is potentially an ultimate “golden bullet” to calm down housing fever and narrow the inequality gap as well as provide sustainable revenue sources for the local governments. In the US, property tax accounted for 33.1 percent of total tax revenues for the state and local government in 2011, according to the US Department of Commerce. Two cities, Shanghai and Chongqing, were selected in 2011 as experiments for collecting property taxes. The pilot programs are not that successful because the tax has a very narrow scope, applying to a limited number of high-end new apartments, and low rates of collection.

We expect the property tax to be expanded nationwide as early as the second half of 2014 in China, after the nationwide housing information system is established. Currently 60 cities are enrolled in the system already. More pilot cities such as Hangzhou, Changsha and Shenzhen could be chosen this year. The following features are expected:

- Annual tax rates are set between 0.5 to 2 percent per annum, possibly with difference among cities based on various factors including need to control property prices, affordability of housing, GDP per capita.

- Taxes likely to be levied on new deals rather than made retroactive, or on the third housing purchase. Transactions of second-hand homes are likely to be regarded as new deals.

- Possible progressive tax rates on multiple property ownership.

Rebalance local government expenditure

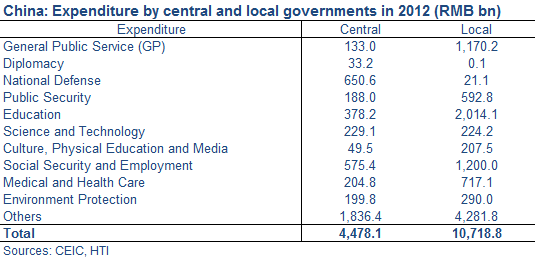

“Pay as you go” should be set as the golden rule for the local governments especially for those with high leverages. Rebalancing local and the central government expenditure is another direction to curb local debts. There is a notable disparity existing between central and local governments in China regarding distribution of revenue and expenditures. In generally, China central and local governments share tax revenues 50-50 but the spending proportions are 30-70 respectively. This gap means that local governments must utilize other sources of finance to make up the difference. This situation has lasted for two decades after China’s tax sharing reforms in 1994. The government therefore should rebalance expenditures more toward central government spending, especially in the areas such as public services, education, social security, medical and health care and environment protections, where the local governments have significantly outspent the central government.

Prerequisites to be Fulfilled

Transparent government budgets

The local governments need to provide the public with more accurate information regarding their spending plans, as well as the usage of proceeds from bonds issuance. Excessive spending by government officials and overpriced products in government procurement have long been criticized by the public in China. For example, annual spending on vehicles, receptions and overseas trips often accounts for 20 to 30 percent of total government spending. Publicly available budget data of local governments is critical for creating healthy public finances in the long run. On August 21 this year, the Ministry of Finance announced that all local governments at the town level or above are required to publish annual budgets by 2015, including details on expenditures of vehicles, receptions and overseas trips.

Sound technical infrastructure

There is also a need to establish technical infrastructure, including a credible and transparent credit rating system, a bond derivative market for more efficient pricing and a better supervision system with automatic mechanisms for correction in the case failure to meet debt criteria. China’s bond future market is to launch on September 6th after being suspended for 18 years. Its underlying asset will be 5 year treasury bonds with face value of 1 million renminbi. The relaunch of government bond futures is expected to boost the trading volume of treasuries and offers a guideline for future bond derivatives.

Conclusion

Auditing local government debts is the very first step towards rebalancing local government fiscal positions. Local government debts may be as high as 40 to 60 percent of GDP, but remain manageable given sizable government assets and revenues. Short-term measures are needed to deleverage cities with large debts, while long-term measures are required to create a more sustainable local government fiscal environment. Resolving this issue provides an opportunity for the government to push forward much-needed structural reforms.